🚢 Japan once built 40% of the world's ships. Then, pushed aside by China and South Korea, that shipbuilding powerhouse saw its global share fall to just 8%. Now the government has drawn up a "Shipbuilding Revival Roadmap," channeling about 1 trillion yen ($6.5 billion) in public and private investment. Industry consolidation, warship exports, and cooperation with the U.S. are all providing tailwinds. Can Japan's shipbuilding industry truly come back? Here's the full picture.

From Global Dominance to an 8% Market Share

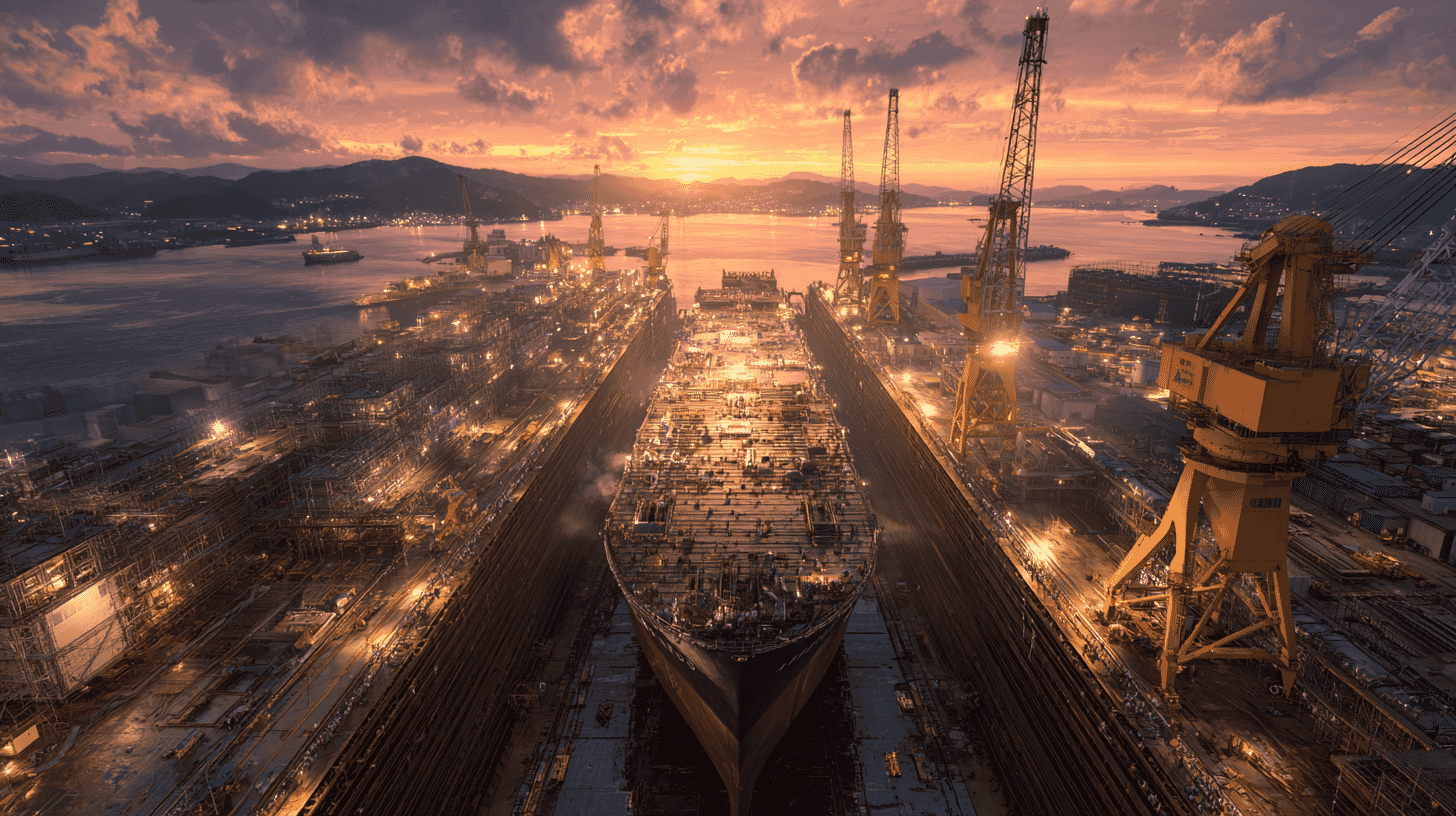

Japan's shipbuilding industry has a history of world dominance. In the 1990s, Japan accounted for about 40% of global ship construction—a true shipbuilding powerhouse. Along the Seto Inland Sea, shipyards launched giant tankers and container ships one after another, a symbol of Japanese manufacturing.

But in the 2000s, everything changed. China nurtured shipbuilding as national policy, growing fast on the back of massive subsidies and low-cost labor. South Korea's conglomerates, such as Samsung Heavy Industries and Hyundai Heavy Industries (now HD Hyundai), dominated the market with large LNG carriers and ultra-large container ships.

As a result, by national share of the world's 2024 shipbuilding orders, China took over 70%, South Korea about 14%, and Japan just 8%. Japan's annual output also fell from about 16 million gross tons in 2019 to roughly 9 million in 2024. Unable to build all the ships its own owners need at home, Japan has relied on Chinese yards for 30–40% of orders since 2022.

The Roadmap: Japan Strikes Back

To break out of this crisis, the Ministry of Land, Infrastructure, Transport and Tourism and the Cabinet Office drew up and released the "Shipbuilding Revival Roadmap" on December 26, 2025. The goal is clear: by 2035, roughly double Japan's annual building capacity to 18 million gross tons. In doing so, the plan aims to recover Japan's global share—eroded by China and South Korea—to around 20%.

To get there, the plan calls for about 1 trillion yen ($6.5 billion) in combined public and private investment. The government will provide roughly 380 billion yen, centered on a "Shipbuilding Revival Fund" aiming for a total of 350 billion yen over ten years; the fiscal 2025 supplementary budget allocated an initial 120 billion yen. Another 12 billion yen goes to an economic-security key-technology program, and 15 billion yen to R&D on AI-driven next-generation shipbuilding robots. The private industry is expected to invest about 350 billion yen in facilities, and the remaining roughly 280 billion yen will fund zero-emission ship production facilities through public-private cooperation using GX (green transformation) economy-transition bonds.

The roadmap also calls for consolidating the industry into one to three groups by around 2028—cutting costs by about 10% while lifting productivity through digitalization, robotics, and AI. The process, however, is still at an early stage; the details of how to bundle public and private investment are to be worked out separately in 2026.

Mega-Merger: Japan's New Shipbuilding Giant

Alongside the roadmap, another development shook the industry: top builder Imabari Shipbuilding making second-ranked Japan Marine United (JMU) a subsidiary.

Announced in June 2025, the deal closed in January 2026. Imabari acquired shares from JFE Holdings and IHI, raising its stake in JMU to 60%. Combined, the two form a shipbuilding group ranking around fourth in the world, accounting for over half of Japan's domestic output.

The significance goes beyond scale. Imabari is strong in mass-produced merchant ships like tankers and bulk carriers, while JMU has technical strength in high-value ships such as escort vessels. It fuses the "power to build in volume" with the "power to win on technology." Moves to share design and procurement are accelerating too, with three major shipping firms investing in a ship-design company jointly founded by Mitsubishi Heavy Industries and Imabari.

Historic Warship Export: Japan's Frigate Goes to Australia

Another development not to be missed is the selection of the enhanced Mogami-class frigate—the fiscal 2024 escort vessel (4,800-ton type), also called the "New FFM"—as the Australian Navy's next-generation general-purpose frigate. Announced by the Australian government on August 5, 2025, it marks Japan's first postwar co-development, production, and transfer of a major defense platform. Mitsubishi Heavy Industries is the prime contractor.

Australia plans to acquire 11 frigates, with the first three built in Japan and the remaining eight in Australia. The program is allocated about 10 billion Australian dollars (roughly 960 billion yen) over ten years, with the first ship targeted for delivery in 2029 and entry into service in 2030.

Australia chose Japan for the New FFM's stealth, long-range capability, and ability to operate with fewer crew than conventional frigates—and, above all, for Japanese shipyards' record of delivering on schedule. Australia's previous frigate program, the British-designed Hunter class, had been plagued by design-change delays and ballooning costs, which strengthened the Japanese bid. The final contract is expected to be signed in 2026.

US-Japan Shipbuilding Cooperation: A New Strategic Pillar

Another reason Japan's shipbuilding is drawing attention is progress in U.S.-Japan cooperation.

The United States maintains the world's most powerful navy, yet its domestic shipbuilding capacity has declined sharply. Repair and maintenance of warships face chronic delays, and in merchant shipbuilding it lags far behind China's capacity.

Against this backdrop, on October 28, 2025, Japanese transport minister Yasushi Kaneko and U.S. Commerce Secretary Howard Lutnick signed a memorandum on U.S.-Japan shipbuilding cooperation. Repairing U.S. warships in Japan and sharing shipbuilding technology are expected to take shape over time—a pillar that could secure steady demand and help Japan maintain its technical edge.

The Challenges That Could Sink the Plan

For all the tailwinds, the challenges pile up.

First, a serious labor shortage. Shipbuilding is labor-intensive and depends on skilled welders and pipe-fitters, but an aging, shrinking population makes it hard for rural yards to recruit young workers. The roadmap calls for stronger industry-academia-government and regional ties, plus expanded acceptance of foreign workers through the Specified Skilled Worker system and the Employment for Skill Development system launching in April 2027.

Second, the scale barrier. Japan's yards are smaller than their Chinese and Korean rivals and struggle to build multiple large ships at once, a cost disadvantage. Achieving the targeted 10% cost cut will require productivity gains through digitalization, robots, and AI.

Third, the question of large LNG carriers, which Japan has not built domestically in recent years. LNG ships demand advanced technology and are dominated by South Korea. The roadmap says it will study future supply-chain commitments, but conclusions are yet to come.

A Turning Tide

From 2026 on, global demand for new ships is expected to peak. As international shipping's decarbonization rules tighten, demand should surge for replacing conventional vessels with eco-friendly, next-generation ships.

As of the end of 2025, Japan's yards held an order backlog of 622 ships and about 30.01 million gross tons—more than three years' worth. New-ship talks are already moving to delivery dates in 2029 and beyond.

Keiji Tanaka, chairman of the Cooperative Association of Japan Shipbuilders, said at a January 2026 New Year gathering that "this year is a 'fair wind,' and we want to raise our sails to catch it." Shipbuilding has long construction times and a broad base, from parts and materials makers to port infrastructure, with major ripple effects on regional economies and jobs where yards are located. Will the government's 1-trillion-yen investment end as a mere slogan, or truly revive the industry? Aligning the sequence of orders, facilities, and people—the patient, unglamorous coordination—will be the test of the next decade.

In Japan, hope for a shipbuilding revival mixes with anxiety over whether the gap with China and South Korea can be closed. What is the state of shipbuilding or the maritime industry in your country? What do you think about government support for industry? Please tell us in the comments.

Global Discussion

15 comments